Audited results for the year ended 31 December 2025

MTN NIGERIA RELEASES AUDITED FINANCIAL RESULTS FOR THE YEAR ENDED

31 DECEMBER 2025

Lagos | Nigeria: 26 February 2026

MTN Nigeria Communications Plc releases financial results for the year ended 31 December

“Strong earnings and cash flow | Resilient balance sheet and resumption of dividends”

Salient points:

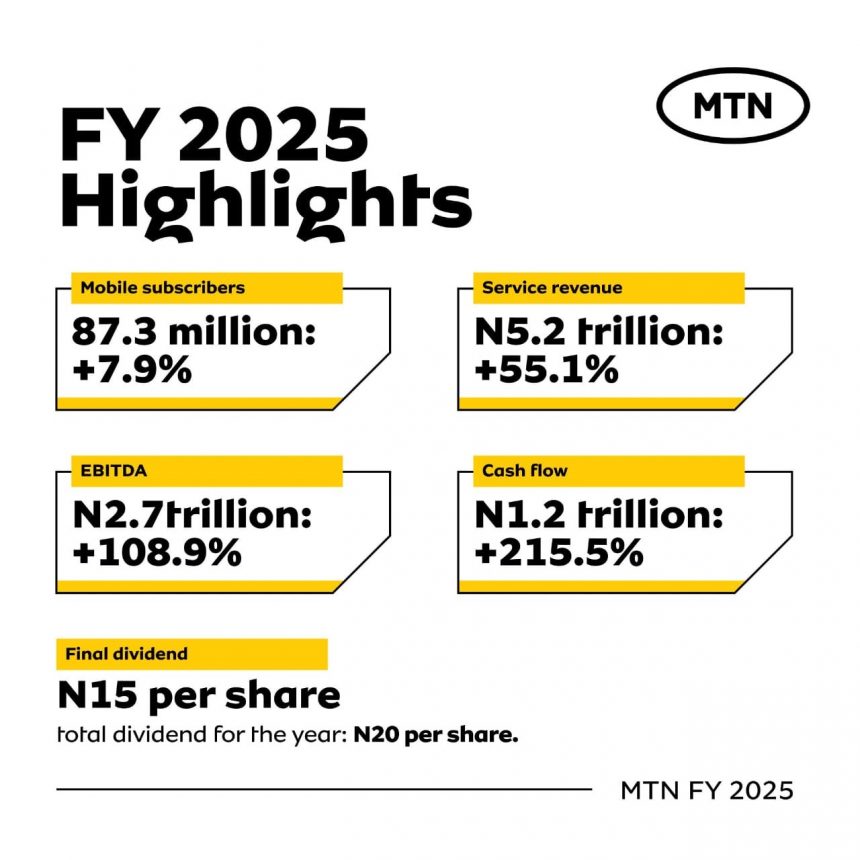

- Total subscribers increased by 7.9% to 87.3 million

- Active data users increased by 11.6% to 53.2 million

- Service revenue increased by 55.1% to N5.2 trillion

- EBITDA increased by 108.9% to N2.7 trillion

- EBITDA margin increased by 13.6pp to 52.7%

- PAT of N1.1 trillion, up 377.9% (FY 2024: negative N400.4 billion)

- Earnings per share of N53.07 kobo (FY 2024: negative N19.05 kobo)

- Retained earnings and shareholders’ equity of N400.4 billion and N548.7 billion,

respectively - Capex, excluding leases, more than doubled to N1 trillion with a capex intensity of 19.3%

- Free cash flow (FCF) of N1.2 trillion, up 215.5%

- Final dividend of N15 per share

- Medium-term guidance:

We maintain an average service revenue growth target of “at

least the low 20%” and revise EBITDA margin upward from the 53-55% range to ‘mid to

high 50%’.

Unless otherwise stated, financial and non-financial information is year-on-year (YoY, 2025 versus 2024).

EBITDA – earnings before interest, tax, depreciation and amortisation

pp – percentage points

PAT – profit after tax

Capex – capital expenditure

Free cash flow – EBITDA less cash-related capex and accounting for working capital movements, income tax and

interest paid

CEO’s Commentary – Karl Toriola:

“2025 marked a significant turning point in our business

performance and resumption of dividend payments. In the period, we returned to profitability,

generated stronger free cash flow and restored positive retained earnings and shareholders’

funds. Our balance sheet resilience was driven by the robust performance of the business as

well as a focused reduction in foreign currency exposure and financial discipline.

These results were delivered through excellent commercial execution, commitment to

operational efficiency and disciplined capital allocation, underpinned by a supportive

macroeconomic environment.

Improved macro conditions

Macroeconomic conditions improved further in 2025 with a more stable foreign exchange

market, improved FX liquidity and a sustained decline in inflation compared to 2024.

The naira strengthened to N1,436/US$ by year-end (2024: N1,535/US$), while tight monetary

policy helped reduce headline inflation to 15.2% (2025 average: 23.4%), partly reflecting

consumer price index (CPI) rebasing. These factors, supported by our tower lease contract

renegotiation, substantially reduced the pressure on our margins, laying a strong foundation

for sustainable cash generation and shareholder returns.

Creating shared value for stakeholders

As part of our goal of building sustainable societies, we expanded broadband coverage by

1.1pp to 91.2% through our network investments – a foundation for productivity, inclusion, and

growth. Through the MTN Nigeria Foundation, we committed N2.7 billion to youth

empowerment, digital inclusion and national development.

We also strengthened Nigeria’s digital skills pipeline by supporting the Federal Ministry of

Communications, Innovation and Digital Economy’s 3 Million Technical Talent (3MTT)

programme. The rehabilitation of the 110-km Enugu–Onitsha Expressway under the Road

Infrastructure Tax Credit Scheme continues to advance, with additional tax credits secured to

offset tax liabilities from 2026.

During the period, we paid N878.7 billion in taxes and levies to the government and were

recognised by the Nigeria Revenue Service for tax compliance and transparency,

demonstrating our track record of sound governance.

Strong commercial momentum

We expanded our mobile subscriber base to 87.3 million (up 6.4 million) and the number of

active data users to 53.2 million (up 5.5 million). The structural demand for data in Nigeria was

demonstrated by the 34.0% increase in data traffic on our network that underpinned our strong

service revenue growth in the period.

We more than double the investment in our network to N1 trillion in 2025 (2024: N443.5 billion),

strengthening service quality and user experience in line with our commitment to our

customers and the government, while positioning our business for growth in an increasingly

data-driven market. We secured a three-year spectrum lease with T2 Mobile, effective 1

October 2025, as part of our national roaming agreement.

These interventions accommodated rising traffic while maintaining a stable, reliable customer

experience. As a result, we were recognised as Nigeria’s best mobile network at the 2025 Ookla

Speedtest Awards, along with other independent crowdsourced benchmarks that continued to

validate our leadership in speed and latency.

Robust trajectory in profitability and strengthened financial position

We delivered robust, broad-based growth across our connectivity and platform businesses,

resulting in a strong topline performance. Service revenue grew by 55.1% (Q4 2025: 49.3%).

Excluding the once-off USSD revenue recognition in Q4 2024, Q4 2025 service revenue

sustained a strong underlying growth of 62.0%. Data remained the primary growth engine,

complemented by solid contributions from voice, fintech and digital services.

Cost pressures were contained through our expense efficiency programme, supported by

moderated inflation and the strengthening of the naira against the dollar. As a result, EBITDA

more than doubled, rising 108.9% to N2.7 trillion, with a margin expansion of 13.6pp to 52.7%,

in line with guidance.

We reported a PAT of N1.1 trillion, up 377.9%, which marked a strong turnaround from the

N400.4 billion after-tax loss in the prior year, supporting the restoration of positive retained

earnings and shareholders’ equity. Our free cash flow of N1.2 trillion was 215.5% higher,

demonstrating robust underlying cash generation, even as we accelerated our capex

deployment in alignment with our quality-of-service and growth objectives.

The Board has proposed a final dividend of N15 per share, payable from distributable net

income, subject to shareholder approval at the Annual General Meeting. This brings the total

dividend for the year to N20 per share, reflecting our ongoing commitment to sustainable value

creation.

Outlook

Looking ahead, we are encouraged by the trajectory of our business as we seek to consolidate

the significant gains achieved in 2025. The favourable macroeconomic environment, our

disciplined execution and continued network leadership position us well for sustained growth

across our connectivity and platform businesses.

Our commitment to operational excellence and disciplined capital allocation will remain

steadfast, ensuring that we progressively strengthen our balance sheet. We remain focused

on driving profitable growth, reinforcing our financial strength and providing consistent

returns to our shareholders.”

Performance highlights

Items

FY 2024 YoY Q4 2025 Q4 2024

5,202,957 3,358,461 54.9% 1,471,954 988,224 48.9%

Service Revenue 5,172,462 3,334,910 55.1% 1,464,217 980,523 49.3%

Data 2,782,006 1,594,362 74.5% 804,766 452,649 77.8%

Voice 1,850,092 1,302,123 42.1% 502,541 352,690 42.5%

Digital 99,426 73,097 36.0% 28,236 22,911 23.2%

Fintech 191,273 106,455 79.7% 59,657 30,148 97.9%

Other Service Revenue 249,665 258,873 (3.6%) 69,017 122,126 (43.5%)

Non-Service Revenue* 30,495 23,551 29.5% 7,737 7,700 0.5%

Other income 1,672 2,369 (29.4%)- 2,369 (100.0%)

Expenses (2,460,864) (2,047,431) (20.2%) (646,424) (537,349) (20.3%)

Cost of Sales (688,269) (528,185) (30.3%) (185,280) (145,225) (27.6%)

Operating Expenses (1,772,595) (1,519,246) (16.7%) (461,144) (392,124) (17.6%)

EBITDA 2,743,765 1,313,399 108.9% 825,530 453,243 82.1%

EBITDA Margin 52.7% 39.1% 13.6pp 56.1% 45.9% 8.8pp

Depreciation & Amortisation (664,254) (535,155) (24.1%) (187,799) (150,305) (24.9%)

Net Finance Costs (473,750) (403,208) (17.5%) (102,829) (119,206) 13.7%

Net foreign exchange Gain/(Loss) 90,268 (925,361) 109.8% 34,689 (20,430) 269.8%

Profit/(Loss) Before Tax 1,696,029 (550,325) 408.2% 569,591 163,302 248.8%

Taxation (583,183) (149,890) (289.1%) (206,928) (48,809) (324.0%)

Profit/(Loss) after Tax 1,112,846 (400,435) 377.9% 362,663 114,493 216.8%

Profit/Loss attributable to:

Owners of the company 1,112,846 (399,448) 378.6% 362,663 114,493 216.8%

Non-controlling interest- (987) 100.0%- –

Profit/(Loss) after Tax 1,112,846 (400,435) 377.9% 362,663 114,493 216.8%

Capital Expenditure 1,596,160 1,531,960 4.2% 345,568 162,888 112.2%

Capital Expenditure excluding Right of Use Assets 1,003,050 443,484 126.2% 245,631 225,845 8.8%

Capex Intensity excluding Right of Use Assets 19.3% 13.2% 6.1pp 16.7% 22.9% (6.2pp)

Free Cash Flows 1,224,850 388,213 215.5% 482,227 (147,872) 426.1%

Mobile Subscribers 87.3 80.9 7.9% 87.3 80.9 7.9%

Data Subscribers 53.2 47.7 11.6% 53.2 47.7 11.6%

MoMo Wallets 3.7 2.8 30.8% 3.7 2.8

*Includes revenue from the sale of devices and SIM cards

Segment performance

Data revenue increased by 74.5%, making it the largest contributor to service revenue. This

growth was supported by an expanded active user base, increased usage and higher traffic.

The number of active data subscribers grew by 11.6%, while smartphone penetration rose by

7.9pp to 66.1%, reflecting the rising demand for high-speed connectivity.

Data traffic increased by 34.0% and average usage per subscriber rose by 20% to 13.1GB. In

addition, 4G population coverage improved by 2.1pp to 84.6%. These results underscore the

effectiveness of our accelerated network investments and our commitment to delivering a

superior quality of service and user experience.

Home broadband remains central to our data growth strategy. By prioritising fixed wireless

access (FWA) and fibre-to-the-home (FTTH), we efficiently serve growing household demand

while deepening our leadership in home connectivity. We introduced unlimited 5G and 1 Gbps

FTTH plans to raise the bar on performance and value for home connectivity. FTTH remain a

core investment priority as demand for high-quality home connectivity accelerates. In 2025,

we added approximately 1 million users, bringing our home broadband subscriber base to 4.2

million.

Voice revenue increased by 42.1%, demonstrating resilience amid elasticity dynamics,

supported by base growth and ongoing customer value management (CVM) initiatives.

Digital revenue grew by 36.0%, led by mobile advertising and content partnerships. We

continued to enhance our digital storefronts and migrated traffic to more modern

engagement platforms, laying the groundwork for more consistent growth in 2026.

Enterprise business delivered revenue growth of 7.7% (up 22.7% excluding the once-off USSD

revenue recognition in Q4 2024), with strong contributions from fixed connectivity, data

services and converged solutions. We commenced monetisation of the Dabengwa Data

Centre, onboarded the first set of customers to the MTN Cloud marketplace and built public

sector partnerships focused on digital transformation use cases.

Fintech revenue grew by 79.7%, supported by higher interest income from deposits and the

continued expansion of advanced services. Active wallets expanded to 3.7 million by

December 2025, following a targeted H2 push that deepened rural penetration, stabilised the

app experience, intensified agent and merchant activations, and strengthened digital CVM.

Float income also increased in line with higher balances, as customer deposits rose 156.1%

from December 2024.

These outcomes demonstrate the momentum in our fintech strategy and the significant

value-creation potential of our platform. As we continue to scale our ecosystem, enhance

product reliability and deepen customer engagement, we are building strong momentum for

sustained fintech growth.

Financial review

Topline growth was driven by a robust execution and pricing discipline. Data now accounts

for more than half of total revenue; voice remains a resilient second pillar, while fintech and

digital provide additional growth vectors.

Cost of sales rose by 30.3%, significantly below revenue growth, lifting gross margin. The

increase in operating expenses was contained to 16.7% and well below revenue growth,

reflecting continued progress in our underlying expense efficiency programme and the

structural savings from the IHS contract renegotiation, generating combined savings of

N288.7 billion in 2025.

As a result, EBITDA more than doubled to N2.7 trillion, with an EBITDA margin up by 13.6pp

to 52.7% (Q4 2025: 56.1%), in line with our guidance of delivering ‘at least the low-50%’. This

highlights disciplined execution and strong operating leverage in our business.

Depreciation and amortisation increased by 24.1%, primarily due to higher right-of-use

assets following the revised tower lease agreements. Net finance costs rose by 17.5%,

reflecting increased lease liabilities resulting from the extended tower lease arrangements.

The quality of our earnings improved significantly in the period under review. We reported a

net foreign exchange gain of N90.3 billion, compared to a loss of N925.4 billion in 2024,

driven by the full settlement of our outstanding letters of credit, a reduction in

foreign-currency loans to US$105 million (2024: US$146 million) and a more stable FX market.

These factors reflect disciplined balance-sheet management and a deliberate strategy to

reduce FX sensitivity and funding risk.

As a result, we closed the year with positive retained earnings of N400.4 billion (December

2024: negative N607.5 billion) and shareholders’ equity of N548.7 billion (December 2024:

negative N458.0 billion).

Reported capex increased marginally by 4.2% due to prior-year lease modifications following

the IHS tower extensions. On an underlying basis (ex-leases), capex rose 126.2%, with capex

intensity at 19.3% – within our target range of ‘high teens’. We invested in core capacity

enhancement, radio densification and spectrum optimisation to ease congestion; new sites to

extend coverage; selective FTTH rollouts in attractive corridors; and a new data centre to

support data and digital growth.

Our capital allocation remained disciplined – protecting network leadership and profitable

growth while managing FX exposure, optimising funding and preserving liquidity. Despite

elevated investment and repayment of a large portion of our debt, free cash flow reached

N1.2 trillion (up 215.5%), which helped to strengthen our balance sheet and demonstrate the

quality of our earnings.

Our funding and liquidity position remained strong. We closed the year with a positive net

cash position of N104.8 billion (2024: negative N719.5 billion). During the period, we repaid

N434.0 billion in facilities (down 45%), including the full settlement of all outstanding

commercial papers, without additional borrowing. Because repayments were weighted to

naira instruments, the naira share of borrowings declined modestly to 71% (December 2024:

73%). We also contained FX exposure in absolute terms through the settlement of US$ LC

obligations and a reduction in our US$ loan balance.

This disciplined approach to deleveraging strengthened our balance sheet resilience and

improved our funding efficiency. Overall, we remain well-positioned with ample liquidity and

disciplined capital management.

Our leverage and coverage metrics remained comfortably within covenants: net

debt-to-EBITDA of negative 0.1x (reflecting our positive net cash position) versus a 2.5x cover

maximum, and interest cover of 26.5x versus a 5x minimum as at December 2025. These

fundamentals underscore our capacity to pursue our growth ambitions while preserving the

flexibility to navigate a dynamic macro environment.

Outlook

Building on the strong recovery in 2025 – marked by a return to profitability, restoration of

positive retained earnings and equity balances and the resumption of dividends – we enter

2026 with optimism and a focus on disciplined execution.

While global geopolitical developments pose some risk to our operating environment and

outlook, we are encouraged by the improved macroeconomic backdrop in Nigeria, supported

by ongoing policy implementation. This provides a more supportive foundation for our

business.

Our investment thesis remains compelling, underpinned by sustained growth in data

consumption and our commitment to network leadership, superior customer experience and

disciplined capital allocation. As part of our broader connectivity strategy, we see opportunity

in the home broadband, where we aim to “own the home” through economically driven FTTH

deployment and rapid FWA scaling. We will balance cost, feasibility, demand and execution

speed to deliver best-in-class connectivity at scale.

We will also continue to scale our platforms. In fintech, our main goals are to scale MoMo

PSB’s active user base, deepen financial inclusion and drive economic impact across Nigeria.

We aim to drive advanced services, including digital payments, by providing seamless,

accessible, and secure financial services, while also enhancing monetisation through CVM

initiatives. In digital infrastructure, we will build on our new data centre capabilities to serve

enterprise and public-sector demand, leveraging artificial intelligence to enhance reliability,

productivity, and cost efficiency under robust governance.

Our financial position provides us with the flexibility to fund growth and returns. Liquidity

remains strong and our exposure to foreign exchange risks has been significantly reduced.

We will maintain this resilience by actively managing currency risk, optimising funding, and

maintaining prudent leverage as we invest to meet rising demand. Our capital allocation will

remain disciplined, prioritising investments that protect our market leadership, support cash

generation, and align with our dividend policy.

In terms of our medium-term guidance framework, we maintain our target average service

revenue growth of “at least the low 20%”, as the impact of price adjustments becomes fully

annualised by Q2 2026. Additionally, we revise EBITDA margin upward from the 53-55% range

to ‘mid to high 50%’. This is based on current economic assumptions, including average

inflation rates remaining within the mid-teens and exchange rates in the N1,400-1,700/US$ range.

Execution will be anchored in disciplined capital expenditures, cost efficiency, and cash

conversion, enabling ongoing investments across connectivity and platforms.

We remain confident in our ability to adapt swiftly, capitalise on emerging opportunities and

deliver sustainable long-term value for our shareholders while advancing inclusive digital

progress across Nigeria.

Karl Olutokun Toriola

Chief Executive Officer

Contact

Chima Nwaokoma

Snr. Manager, Investor Relations

MTN Nigeria Communications Plc

Telephone: +234 803 200 0186

Email: investorrelations.ng@mtn.com

About MTN Nigeria

Funso Aina

Snr. Manager, External Relations

MTN Nigeria Communications Plc

Telephone: +234 803 200 4168

Email: mediaenquiries.ng@mtn.com

MTN Nigeria is one of Africa’s largest providers of communications services, connecting over

85 million people in communities across the country with each other and the world. Guided by

a belief that everybody deserves the benefits of a modern connected life, MTN Nigeria’s

leadership position in coverage, capacity, and innovation has remained constant since its

launch in 2001. MTN Nigeria is part of the MTN Group – a multinational telecommunications

group which operates in 16 countries in Africa and the Middle East, serving over 300 million

people.

Visit www.mtn.ng for more information

Stay ahead with the latest updates!

Join The Podium Media on WhatsApp for real-time news alerts, breaking stories, and exclusive content delivered straight to your phone. Don’t miss a headline — subscribe now!

Chat with Us on WhatsApp