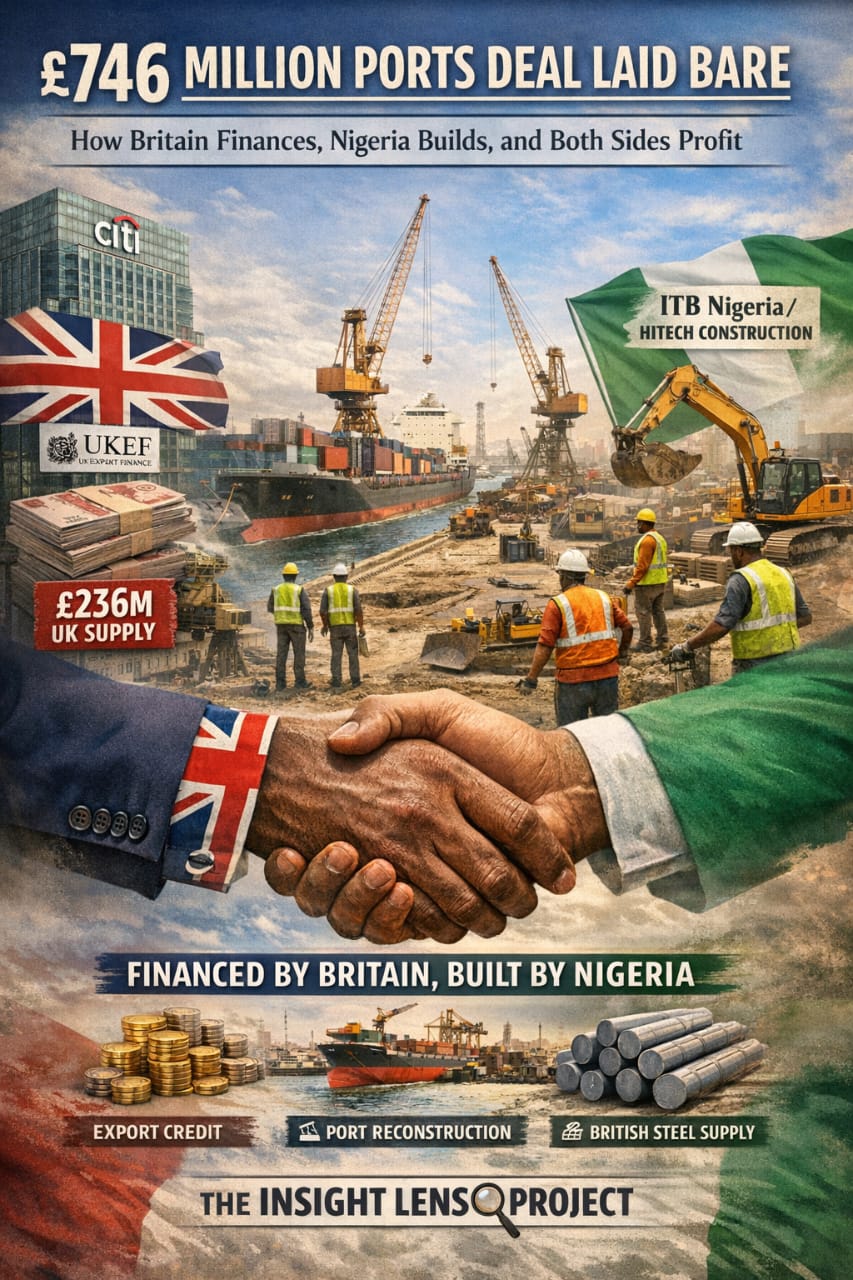

Contrary to the popular narrative, no single company sits at the centre of Nigeria’s £746 million ports refurbishment deal. It is not a turnkey contract handed to a foreign firm, but a layered arrangement built around government-backed export finance, with distinct roles for financiers, contractors and suppliers.

At the heart of the transaction is a Buyer Credit Facility structured by Citibank, acting through its London branch. The bank serves as the principal commercial arranger, coordinating lenders, structuring the loan and managing documentation between Nigeria’s finance authorities and participating institutions. Its role is crucial, without such structuring, the financing package would not exist in its current form.

Standing behind the loan is UK Export Finance (UKEF), the British government’s export credit agency, which provides a full sovereign guarantee. This guarantee effectively removes much of the risk for lenders, enabling Nigeria to access long-term financing on more favourable terms than would otherwise be available. The arrangement, formally witnessed at state level, underscores that this is a government-to-government backed facility, not a private concession.

The actual reconstruction of Lagos’s Apapa and Tin Can Island ports tells a different story, one rooted firmly in domestic execution. The civil works contract, awarded earlier in 2025 before the financing was finalised, sits with ITB Nigeria, a subsidiary of the Chagoury Group. The firm, long established in Nigeria’s infrastructure space, is responsible for the physical delivery of the project, from rehabilitation works to installation of equipment.

ITB Nigeria is working alongside Hitech Construction Africa, another company linked to the same industrial network. Together, they form the operational backbone of the project, handling execution on the ground. This distinction is crucial, while the financing carries a strong international imprint, the delivery remains in Nigerian hands.

British involvement, though prominent in headlines, is concentrated on the supply side rather than construction. British Steel has secured a contract valued at roughly £70 million to supply steel billets required for the works. Other UK firms are expected to benefit from additional supply and equipment contracts, bringing total British participation to about £236 million.

This allocation is not incidental but embedded in the financing structure itself. UKEF’s support comes with a clearly defined condition: at least 20 per cent of the contract value must be sourced from UK companies. In this instance, the share exceeds that threshold, reaching approximately 31.6 per cent. Such requirements fall under UKEF’s Foreign Content Policy, a framework designed to ensure that British industry benefits directly from overseas projects backed by UK guarantees.

This is what gives the arrangement its “tied financing” character. While not as restrictive as older models of tied aid, which mandated total spending in the lending country, it nonetheless guarantees a meaningful return flow to British suppliers. Without meeting this threshold, the UKEF guarantee, and by extension the financing itself would not be available.

Importantly, these rules are not unusual. Export credit agencies across the world, from the United States to China, operate similar frameworks. They are also fully consistent with the OECD Arrangement on Officially Supported Export Credits, which governs financial terms such as interest rates, repayment periods and the widely adopted cap allowing up to 85 per cent of a project’s value to be financed through such facilities. What the OECD does not dictate, however, is domestic content, leaving countries free to set their own thresholds.

Here, the United Kingdom has opted for a relatively flexible approach. Its 20 per cent minimum is modest by international standards, particularly when compared with the far stricter requirements of the United States’ Export-Import Bank, which often demands significantly higher domestic content for full support. The British model, by contrast, is designed to strike a balance, securing opportunities for UK exporters while remaining competitive in global infrastructure financing.

The Nigeria ports deal illustrates this balance in practice. Nigerian firms retain control over execution, while British companies secure a guaranteed slice of the supply chain. The financing structure, meanwhile, ensures that lenders are protected and the borrower gains access to capital on viable terms.

Critics have framed the arrangement as one-sided, arguing that it channels public borrowing into foreign industry. Yet such characterisations overlook the dual nature of the transaction. Nigeria gains critical infrastructure upgrades, long delayed and economically significant, while the UK leverages its financial instruments to support domestic industry. Each side extracts value, even though in different forms.

In the end, the deal is less about hidden actors than about the mechanics of modern export finance. It is a system in which governments, banks and contractors play distinct roles, and where national interest is carefully woven into international cooperation. Whether it proves advantageous for Nigeria will depend not on the structure alone, but on execution, cost efficiency and the long-term impact of the ports themselves.

©️ Adebamiwa Olugbenga Michael is a Lagos-based journalist, political economy, and policy intelligence analyst, and the publisher of The Insight Lens Project, delivering principled, data-driven insights on Nigeria’s political, economic, and social landscape using open-source information across Nigeria and West Africa.

Stay ahead with the latest updates!

Join The Podium Media on WhatsApp for real-time news alerts, breaking stories, and exclusive content delivered straight to your phone. Don’t miss a headline — subscribe now!

Chat with Us on WhatsApp

{kind=link}